SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| x PreliminaryProxy Statement |

¨ Confidential, for Use of the Commission Only(as Permitted by Rule 14a-6(e)(2)) | |

| ¨ Definitive Proxy Statement |

||

| ¨ Definitive Additional Materials |

||

| ¨ Soliciting Material Pursuant to §240.14a-11(c) or §240.14a-12 | ||

Equinix, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

x No fee required.

¨ Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11.

| 1. | Title of each class of securities to which transaction applies: |

| 2. | Aggregate number of securities to which transaction applies: |

| 3. | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): |

| 4. | Proposed maximum aggregate value of transaction: |

| 5. | Total fee paid: |

¨ Fee paid previously with preliminary materials:

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| 1. | Amount Previously Paid: |

| 2. | Form, Schedule or Registration Statement No.: |

| 3. | Filing Party: |

| 4. | Date Filed: |

Notes:

EQUINIX, INC.

301 Velocity Way, Fifth Floor

Foster City, CA 94404

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To be held June 3, 2003

The Annual Meeting of Stockholders (the “Annual Meeting”) of Equinix, Inc. (the “Company”) will be held at the Company’s headquarters located at 301 Velocity Way, Fifth Floor, Foster City, California, on Tuesday, June 3, 2003, at 10:30 a.m. for the following purposes:

1. To elect eight (8) directors of the Board of Directors to serve until the next Annual Meeting or until their successors have been duly elected and qualified;

2. To ratify the appointment of PricewaterhouseCoopers LLP as the Company’s independent accountants for the fiscal year ending December 31, 2003;

3. To approve the issuance of shares of our common stock in connection with a debt financing pursuant to which we will raise $10.0 million; and

4. To transact such other business as may properly come before the meeting or any adjournments or postponements thereof.

The foregoing items of business are more fully described in the attached Proxy Statement.

Only stockholders of record at the close of business on April 29, 2003 are entitled to notice of, and to vote at, the Annual Meeting and at any adjournments or postponements thereof. A list of such stockholders will be available for inspection at the Company’s headquarters located at 301 Velocity Way, Fifth Floor, Foster City, California, during ordinary business hours for the ten-day period prior to the Annual Meeting.

BY ORDER OF THE BOARD OF DIRECTORS,

Peter F. Van Camp

Chief Executive Officer

and Director

Foster City, California

May 16, 2003

IMPORTANT

WHETHER OR NOT YOU PLAN TO ATTEND THE ANNUAL MEETING, PLEASE COMPLETE, SIGN, DATE AND PROMPTLY RETURN THE ACCOMPANYING PROXY IN THE ENCLOSED POSTAGE-PAID ENVELOPE. YOU MAY REVOKE YOUR PROXY AT ANY TIME PRIOR TO THE ANNUAL MEETING. IF YOU DECIDE TO ATTEND THE ANNUAL MEETING AND WISH TO CHANGE YOUR PROXY VOTE, YOU MAY DO SO AUTOMATICALLY BY VOTING IN PERSON AT THE MEETING.

EQUINIX, INC.

301 Velocity Way, Fifth Floor

Foster City, CA 94404

PROXY STATEMENT

FOR ANNUAL MEETING OF STOCKHOLDERS

To be held June 3, 2003

These proxy materials are furnished in connection with the solicitation of proxies by the Board of Directors of Equinix, Inc., a Delaware corporation (the “Company”), for the Annual Meeting of Stockholders (the “Annual Meeting”) to be held at the Company’s headquarters located at 301 Velocity Way, Foster City, California, on Tuesday, June 3, 2003, at 10:30 a.m., and at any adjournment or postponement of the Annual Meeting. These proxy materials were first mailed to stockholders on or about May 16, 2003.

PURPOSE OF MEETING

The specific proposals to be considered and acted upon at the Annual Meeting are summarized in the accompanying Notice of Annual Meeting of Stockholders. Each proposal is described in more detail in this Proxy Statement.

VOTING RIGHTS AND SOLICITATION OF PROXIES

The Company’s common stock and series A preferred stock are the only type of securities entitled to vote at the Annual Meeting. On April 29, 2003, the record date for determination of stockholders entitled to vote at the Annual Meeting, there were 8,518,790 shares of common stock outstanding and 1,868,667 shares of series A preferred stock outstanding. Each stockholder of record on April 29, 2003 is entitled to one vote for each share of common stock or series A preferred stock held by such stockholder on April 29, 2003. All votes will be tabulated by the inspector of elections appointed for the meeting, who will separately tabulate affirmative and negative votes, abstentions and broker non-votes.

Quorum Required

The Company’s bylaws provide that the holders of a majority of the Company’s common stock and voting preferred stock issued and outstanding and entitled to vote at the Annual Meeting, present in person or represented by proxy, shall constitute a quorum for the transaction of business at the Annual Meeting. Abstentions and broker non-votes will be counted as present for the purpose of determining the presence of a quorum.

Votes Required

Proposal 1. Directors are elected by a plurality of the affirmative votes cast by those shares present in person, or represented by proxy, and entitled to vote at the Annual Meeting. The eight (8) nominees for director receiving the highest number of affirmative votes will be elected. Abstentions and broker non-votes will not be counted toward a nominee’s total.

Proposal 2. Ratification of the appointment of PricewaterhouseCoopers LLP as the Company’s independent accountants for the fiscal year ending December 31, 2003 requires the affirmative vote of a majority of those shares present in person, or represented by proxy, and cast either affirmatively or negatively at the Annual Meeting. Abstentions and broker non-votes will not be counted as having been voted on the proposal.

1

Proposal 3. The approval of the issuance of our stock in connection with the financing requires the affirmative vote of a majority of those shares present in person, or represented by proxy, and cast either affirmatively or negatively at the Annual Meeting. Abstentions and broker non-votes will not be counted as having been voted on the proposal.

Proxies

Whether or not you are able to attend the Company’s Annual Meeting, you are urged to complete and return the enclosed proxy, which is solicited by the Company’s Board of Directors and which will be voted as you direct on your proxy when properly completed. In the event no directions are specified, such proxies will be voted FOR the nominees of the Board of Directors (as set forth in Proposal 1), FOR Proposal 2, FOR Proposal 3, and in the discretion of the proxy holders as to other matters that may properly come before the Annual Meeting. You may also revoke or change your proxy at any time before the Annual Meeting. To do this, send a written notice of revocation or another signed proxy with a later date to the Secretary of the Company at the Company’s principal executive offices before the beginning of the Annual Meeting. You may also automatically revoke your proxy by attending the Annual Meeting and voting in person. All shares represented by a valid proxy received prior to the Annual Meeting will be voted.

Solicitation of Proxies

The Company will bear the entire cost of solicitation, including the preparation, assembly, printing, and mailing of this Proxy Statement, the proxy, and any additional soliciting material furnished to stockholders. Copies of solicitation material will be furnished to brokerage houses, fiduciaries, and custodians holding shares in their names that are beneficially owned by others so that they may forward this solicitation material to such beneficial owners. In addition, the Company may reimburse such persons for their costs of forwarding the solicitation material to such beneficial owners. The original solicitation of proxies by mail may be supplemented by solicitation by telephone, telegram, or other means by directors, officers or employees. No additional compensation will be paid to directors, officers or employees for such services.

2

PROPOSAL 1

ELECTION OF DIRECTORS

The directors who are being nominated for re-election to the Board of Directors (the “Nominees”), their ages as of April 1, 2003, their positions and offices held with the Company and certain biographical information are set forth below. The proxy holders intend to vote all proxies received by them in the accompanying form FOR the Nominees listed below unless otherwise instructed. In the event any Nominee is unable or declines to serve as a director at the time of the Annual Meeting the proxies will be voted for any nominee who may be designated by the present Board of Directors to fill the vacancy. As of the date of this Proxy Statement, the Board of Directors is not aware of any Nominee who is unable or will decline to serve as a director. The eight (8) nominees receiving the highest number of affirmative votes of the shares entitled to vote at the Annual Meeting will be elected directors of the Company to serve until the next Annual Meeting or until their successors have been duly elected and qualified.

| Nominees |

Age |

Positions and Offices Held with the Company | ||

| Lee Theng Kiat |

50 |

Chairman of the Board | ||

| Steven Eng (1) (2) (4) |

46 |

Director | ||

| Scott Kriens (1) (4) |

45 |

Director | ||

| Jean Mandeville |

43 |

Director | ||

| Andrew Rachleff (2) (4) |

44 |

Director | ||

| Dennis Raney (2) |

60 |

Director | ||

| Peter Van Camp (3) |

47 |

Director and Chief Executive Officer | ||

| Michelangelo Volpi (1) |

36 |

Director |

| (1) | Member of Compensation Committee |

| (2) | Member of Audit Committee |

| (3) | Member of Option Committee |

| (4) | Member of Nominating Committee |

Lee Theng Kiat has served as the chairman of the board since December 2002. Mr. Lee has been president and chief executive officer of Singapore Technologies Telemedia Pte. Ltd, an information and communications company, since November 1995. Mr. Lee also serves on the board of directors of Enersave Holdings Limited and Horizon Education & Technologies Limited, both public-listed companies in Singapore, as well as several privately held and non-listed public companies in Singapore.

Steven Eng has served as a director of Equinix since December 2002. Mr. Eng has been a program manager of network management systems at WAM!NET Government Services, Inc. since April 2002. Prior to joining WAM!NET Mr. Eng served as vice president of Exodus Communications from March 1995 to September 2001.

Scott Kriens has served as a director of Equinix since July 2000. Mr. Kriens has been president, chief executive officer and chairman of the board of directors of Juniper Networks, Inc., an Internet infrastructure solutions company, since January 1996. From April 1986 to January 1996, Mr. Kriens served as vice president of sales and vice president of operations at StrataCom, Inc., a telecommunications equipment company, which he co-founded in 1986. Mr. Kriens serves on the board of directors of Verisign, Inc. and Juniper Networks, Inc., both public companies, as well as several privately held companies.

Jean Mandeville has served as a director of Equinix since December 2002. Mr. Mandeville has been the chief financial officer of Singapore Technologies Telemedia Pte. Ltd since July 2002. From January 1998 to June 2002, Mr. Mandeville served in various capacities at British Telecom PLC, including President of Asia Pacific from July 2000 to June 2002, Director of International Development Asia Pacific from June 1999 to July 2000 and GM, Special Projects from January 1998 to July 1999. Mr. Mandeville also served on the board of directors of SmarTone HK and LGT Korea, both public companies, and serves on the board of several privately held companies.

3

Andrew Rachleff has served as a director of Equinix since September 1998. In May 1995, Mr. Rachleff co-founded Benchmark Capital, a venture capital firm, and has served as a general partner since that time. Prior to co-founding Benchmark Capital, Mr. Rachleff spent ten years as a general partner with Merrill, Pickard, Anderson & Eyre, a venture capital firm. Mr. Rachleff also serves on the board of directors of Opsware, Inc. and Blue Coat Systems, Inc. (formerly known as CacheFlow Inc.), both public companies, as well as several privately held companies.

Dennis Raney has served as a director of Equinix since April 2003. Mr. Raney has been the chief financial officer of eONE Global, LP since July 2001. Prior to joining eONE Global, Mr. Raney held the position of chief financial officer and executive vice president at Novell Inc. from March 1998 to July 2001. Mr. Raney also serves on the board of directors of ProBusiness, a public company, and Redleaf Group Inc., a privately held company.

Peter Van Camp has served as Equinix’s chief executive officer and as a director since May 2000. From June 2001 to December 2002, Mr. Van Camp was also chairman of the board. From January 1997 to May 2000, Mr. Van Camp was employed at UUNET, the Internet division of WorldCom, where he served as president of Internet markets and, most recently, as president of the Americas region. During the period from May 1995 to January 1997, Mr. Van Camp was president of Compuserve Network Services, an Internet access provider. Before holding this position, Mr. Van Camp held various positions at Compuserve, Inc. during the period between October 1982 to May 1995. Mr. Van Camp currently serves as a director of Packeteer, Inc., a public company.

Michelangelo Volpi has served as a director of Equinix since November 1999. Mr. Volpi joined Cisco Systems, Inc. (“Cisco”), a data communications equipment manufacturer, in 1994. Currently, he holds the position of senior vice president for Cisco’s Internet switching and services group. Prior to his current position, Mr. Volpi was chief strategy officer for Cisco where he played an instrumental role in the creation of Cisco’s acquisition and investment strategies. Before joining Cisco, Mr. Volpi spent three years at Hewlett Packard’s Optoelectronics Division.

Nomination of Board of Directors

Under the provisions of the Company’s Bylaws, the number of directors is fixed at nine. In addition, the Bylaws provide that, until December 31, 2004, or if earlier, the termination of the governance provisions in the bylaws, (i) three directors shall be nominated by STT Communications; and (ii) three directors, known as the Equinix directors, shall be nominated by the three directors appointed to Equinix’s current Board of Directors by Equinix’s Board of Directors as it existed prior to December 31, 2002. Three directors shall be nominated by the Company’s nominating committee, and must be independent. The three directors nominated by STT are Lee Theng Kiat, Steven Eng and Jean Mandeville. The three directors nominated by the Equinix directors are Andrew Rachleff, Peter Van Camp and Michelangelo Volpi. The directors nominated by the nominating committee are Scott Kriens and Dennis Raney. These governance provisions are more fully described in our definitive proxy statement dated December 12, 2002. There will be one vacancy on the board of directors as of the date of the Annual Meeting. However, proxies can not be voted for a greater number of persons than the eight nominees named herein.

Board of Directors Meetings and Committees

During the fiscal year ended December 31, 2002, the Board of Directors held six (6) meetings and acted by written consent on four (4) occasions. For the fiscal year, each of the directors, during the term of their tenure, attended or participated in at least 75% of the aggregate of (i) the total number of meetings or actions by written consent of the Board of Directors and (ii) the total number of meetings held by all committees of the Board of Directors on which each such director served. The Board of Directors has four (4) standing committees: the Audit Committee, the Compensation Committee, the Nominating Committee and the Option Committee.

4

The Audit Committee of the Company’s Board of Directors (the “Audit Committee”) was created on July 19, 2000. The Audit Committee reviews, acts on and reports to the Board of Directors with respect to various auditing and accounting matters, including the selection of the Company’s independent accountants, the scope of the annual audits, fees to be paid to the Company’s independent accountants, the performance of the Company’s accountants and the accounting practices of the Company. The members of the Audit Committee are Messrs. Eng, Rachleff and Raney. During the fiscal year ended December 31, 2002, the Audit Committee of the Board of Directors held three (3) meetings. In addition, the Audit Committee met once in April 2002 to discuss the results of the previous quarter.

The Compensation Committee of the Company’s Board of Directors (the “Compensation Committee”) was created on July 19, 2000. The Compensation Committee reviews the performance of the executive officers of the Company, establishes compensation programs for the officers, and reviews the compensation programs for other key employees, including salary and cash bonus levels and option grants under the 2000 Equity Incentive Plan, Employee Stock Purchase Plan and 2001 Supplemental Stock Plan. The members of the Compensation Committee are Messrs. Eng, Kriens and Volpi. During the fiscal year ended December 31, 2002, the Compensation Committee of the Board of Directors held no meetings and acted by written consent on five (5) occasions.

The Nominating Committee of the Company’s Board of Directors (the “Nominating Committee”) was created December 30, 2002. The Nominating Committee develops qualification criteria for board members and selects the director nominees for each annual meeting of stockholders in accordance with the Company’s bylaws. Stockholders wishing to recommend candidates for consideration by the Nominating Committee may do so by writing to the Secretary of the Company and providing the candidates name, biographical data and qualifications. The members of the Nominating Committee are Messrs. Eng, Kriens and Rachleff. During the fiscal year ended December 31, 2002, the Nominating Committee held no meetings.

The Option Committee of the Company’s Board of Directors (the “Option Committee”) was created on July 19, 2000. The Board has delegated to the Option Committee the authority to approve the grant of stock options to non-officer employees and other individuals. The sole member of the Option Committee during the 2002 fiscal year was Mr. Van Camp. During the fiscal year ended December 31, 2002, the Option Committee held no meetings and acted by written consent on thirty-three (33) occasions.

Compensation of Directors

Except for grants of stock options, directors of the Company generally do not receive compensation for services provided as a director or for participation on any committee of the Board of Directors. Directors are not reimbursed for their out-of-pocket expenses in serving on the Board of Directors or any committee of the Board of Directors. Non-employee directors are eligible to receive options under the Company’s 2000 Director Option Plan (the “Directors’ Plan”). Each non-employee director receives an option for 7,000 shares of the Company’s common stock upon joining the Board. The option becomes exercisable and vests in four equal annual installments from the date of grant. In addition, at each of the Company’s annual stockholders’ meetings, each non-employee director who will continue to be a director after that meeting will automatically be granted at that meeting an option for 2,500 shares of the Company’s common stock. This option becomes fully exercisable and fully vested on the first anniversary of the date of grant. However, a new non-employee director who is receiving the initial option will not receive the annual option in the same calendar year.

5

The following table sets forth for each of the non-employee directors the number of securities underlying options held by the non-employee directors at December 31, 2002:

| Number of Securities Underlying Unexercised Options at December 31, 2002 |

Weighted Average Exercise Price | ||||||

| Exercisable |

Not Exercisable |

||||||

| Steven Eng |

0 |

7,000 |

$ |

5.70 | |||

| Scott Kriens |

938 |

938 |

$ |

158.86 | |||

| Lee Theng Kiat |

0 |

0 |

|

— | |||

| Jean Mandeville |

0 |

0 |

|

— | |||

| Andrew Rachleff |

938 |

938 |

$ |

158.86 | |||

| Dennis Raney |

0 |

0 |

|

— | |||

| Michelangelo Volpi (1) |

0 |

0 |

|

— | |||

| (1) | Mr. Volpi, in compliance with his employer’s policy regarding compensation in relation to external board positions, has waived his right to any stock grants or other compensation. |

Non-employee directors are also eligible to receive options as well as shares of common stock under the Company’s 2000 Equity Incentive Plan. Directors who are also employees of the Company are eligible to receive options as well as shares of common stock under the Company’s 2000 Equity Incentive Plan and to participate in the Company’s Employee Stock Purchase Plan.

Recommendation of the Board of Directors

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” THE NOMINEES LISTED HEREIN.

Other Executive Officers

The following are additional executive officers of the Company, their ages as of April 1, 2003, their positions and offices held with the Company and certain biographical information. All executive officers serve at the discretion of the Board of Directors.

| Executive Officers |

Age |

Positions and Offices Held with the Company | ||

| Marjorie S. Backaus |

41 |

Chief Marketing Officer and Vice President of Market Strategy | ||

| Peter T. Ferris |

45 |

Vice President, Worldwide Sales | ||

| Brandi L. Galvin |

30 |

General Counsel and Assistant Secretary | ||

| Philip J. Koen |

51 |

President and Chief Operating Officer | ||

| Renée F. Lanam |

40 |

Chief Financial Officer and Secretary | ||

| Keith D. Taylor |

41 |

Vice President, Finance and Chief Accounting Officer |

Marjorie S. Backaus has served as Equinix’s chief marketing officer since November 1999, and as Vice President of Market Strategy since February 2000. During the period from August 1996 to November 1999, Ms. Backaus was vice president of marketing at Global One, an international telecommunications company. From November 1987 to August 1996, Ms. Backaus served in various positions at AT&T, a telecommunications company, including positions in regulatory, product management and strategic alliances.

Peter T. Ferris has served as Equinix’s vice president, worldwide sales since July 1999. During the period from June 1997 to July 1999, Mr. Ferris was vice president of sales for Frontier Global Center, a provider of

6

complex web site hosting services. From June 1996 to June 1997, Mr. Ferris served as vice president, eastern sales at Genuity Inc., an Internet services provider. From December 1993 to June 1996, Mr. Ferris was vice president, mid-Atlantic sales at MFS DataNet Inc., a telecommunications services provider.

Brandi L. Galvin has served as Equinix’s general counsel and assistant secretary since January 2003. Before joining Equinix, Ms. Galvin was employed at the law firm of Gunderson Dettmer Stough Villeneuve Franklin & Hachigian, LLP (“Gunderson Dettmer”), where she was an associate from September 1997 to January 2003.

Philip J. Koen has served as Equinix’s president and chief operating officer since May 2001. From July 1999 to May 2001, Mr. Koen also served as Equinix’s chief financial officer and secretary. In addition, Mr. Koen served as the Company’s corporate development officer from May 2000 to May 2001. Before joining Equinix, Mr. Koen was employed at PointCast, Inc., an Internet company, where he served as chief executive officer during the period from March 1999 to June 1999; chief operating officer during the period from November 1998 to March 1999; and chief financial officer and executive vice president responsible for software development and network operations during the period from July 1997 to November 1998. From December 1993 to May 1997, Mr. Koen was vice president of finance and chief financial officer of Etec Systems, Inc., a semi-conductor equipment company. Mr. Koen currently serves as a director of BlueCoat Systems, Inc., a public company.

Renée F. Lanam has served as Equinix’s chief financial officer and secretary since February 2002, and as general counsel from April 2000 to January 2003. From April 2000 to February 2002, Ms. Lanam also served as Equinix’s assistant secretary. In addition, Ms. Lanam served as vice president of corporate finance from November 2001 to February 2002. Before joining Equinix, Ms. Lanam was employed at Gunderson Dettmer, where she was an associate from January 1996 to January 2000 and a partner from January 2000 to April 2000. Prior to joining Gunderson Dettmer, Ms. Lanam was an associate at the law firms of Jackson, Tufts, Cole & Black and Brobeck, Phleger & Harrison, LLP.

Keith D. Taylor has served as Equinix’s vice president, finance, and chief accounting officer since February 2001. From February 1999 to February 2001, Mr. Taylor served as Equinix’s director of finance and administration. Before joining Equinix, Mr. Taylor was employed by International Wireless Communications, Inc., an operator, owner and developer of wireless communication networks, as vice president finance and interim chief financial officer. Prior to joining International Wireless Communications, Inc., Mr. Taylor was employed by Becton Dickinson & Company, a medical and diagnostic device manufacturer, as a senior sector analyst for the diagnostic businesses in Asia, Latin America and Europe.

7

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

The following table sets forth, as of February 28, 2003, certain information with respect to shares beneficially owned by (i) each person who is known by the Company to be the beneficial owner of more than five percent of the Company’s outstanding shares of common stock, (ii) each of the Company’s directors, (iii) each of the executive officers named in Executive Compensation and Related Information, and (iv) all current directors and executive officers as a group. Beneficial ownership has been determined in accordance with Rule 13d-3 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Under this rule, certain shares may be deemed to be beneficially owned by more than one person (if, for example, persons share the power to vote or the power to dispose of the shares). In addition, shares are deemed to be beneficially owned by a person if the person has the right to acquire shares (for example, upon exercise of an option or warrant) within sixty (60) days of the date as of which the information is provided. In computing the percentage ownership of any person, the amount of shares is deemed to include the amount of shares beneficially owned by such person (and only such person) by reason of such acquisition rights. As a result, the percentage of outstanding shares of any person as shown in the following table does not necessarily reflect the person’s actual voting power at any particular date. Unless otherwise indicated, the address for each listed stockholder is c/o Equinix, Inc., 301 Velocity Way, Fifth Floor, Foster City, California 94404.

| Shares Beneficially Owned |

|||||

| Name of Beneficial Owner |

Number of Shares |

Percentage of Total |

|||

| Peter F. Van Camp (1) |

168,724 |

1.95 |

% | ||

| Albert M. Avery, IV (2) |

83,423 |

* |

| ||

| Steven Poy Eng 51 Cuppage Road #10-11/17 StarHub Centre Singapore 229469 |

0 |

— |

| ||

| Harry F. Hopper III (3) |

498,014 |

5.86 |

% | ||

| Theng Kiat Lee (4) 51 Cuppage Road #10-11/17 StarHub Centre Singapore 229469 |

0 |

— |

| ||

| Renee F. Lanam (5) |

39,411 |

* |

| ||

| Jean F.H.P. Mandeville (6) 51 Cuppage Road #10-11/17 StarHub Centre Singapore 229469 |

0 |

— |

| ||

| Andrew S. Rachleff (7) |

271,429 |

3.19 |

% | ||

| Michelangelo Volpi (8) |

0 |

— |

| ||

| Scott Kriens (9) |

938 |

* |

| ||

| Marjorie S. Backaus (10) |

36,252 |

* |

| ||

| Peter T. Ferris (11) |

37,294 |

* |

| ||

| Entities affiliated with STT Communications Ltd.(12) 51 Cuppage Road #10-11/17 Starhub Centre Singapore 229469 |

4,943,569 |

40.00 |

% | ||

| Entities affiliated with Goldman Sachs (13) 85 Broad Street New York, NY 10004 |

1,042,799 |

12.26 |

% | ||

| All current directors and executive officers as a group (15 persons)(14) |

1,251,117 |

14.41 |

% | ||

| * | Less than 1%. |

| (1) | Includes 162,474 shares subject to options that are exercisable within 60 days of February 28, 2003. |

| (2) | Includes 3,703 shares subject to options that are exercisable within 60 days of February 28, 2003. |

8

| (3) | Represents 310,824 shares of common stock held by Columbia PIXC Partners III, L.L.C., 96,166 shares of common stock held by Columbia PIXC Partners, L.L.C., and 91,024 shares of common stock held by Columbia Capital Equity Partners (QP) L.P. Mr. Hopper is a managing member of Columbia PIXC Partners III, L.L.C. and Columbia PIXC Partners III, L.L.C. Mr. Hopper may be deemed to share voting and investment power with respect to all shares owned by Columbia Capital entities. |

| (4) | Mr. Kiat is President of Singapore Technologies Telemedia Pte. Ltd., which may be deemed to beneficially own 4,596,495 shares which are beneficially owned by STT Communications Ltd., a subsidiary of Singapore Technologies Telemedia Ptc. Ltd., as set forth in footnote 12. |

| (5) | Includes 37,600 shares subject to options that are exercisable within 60 days of February 28, 2003. |

| (6) | Mr. Mandeville is Chief Financial Officer of Singapore Technologies Telemedia Pte. Ltd., which may be deemed to beneficially own 4,596,495 shares which are beneficially owned by STT Communications Ltd., a subsidiary of Singapore Technologies Telemedia Ptc. Ltd., as set forth in footnote 12. |

| (7) | Represents 266,718 shares of common stock held by Benchmark Capital Partners II, L.P., as nominee for Benchmark Capital Partners II, L.P., Benchmark Founders’ Fund II, L.P., Benchmark Founders’ Fund II-A, L.P. and Benchmark Members’ Fund II, L.P., and 3,578 shares of common stock held by Benchmark Capital Partners IV, L.P., as nominee for Benchmark Capital Partners, IV, L.P., Benchmark Founders’ Fund IV, L.P., Benchmark Founders’ Fund IV-A, L.P. and related individuals. Mr. Rachleff is a managing member of Benchmark Capital Management Co. II, LLC, the general partner of Benchmark Capital Partners, II, L.P., Benchmark Founders’ Fund II, L.P. Benchmark Founders’ Fund II-A, L.P. and Benchmark Members’ Fund II, L.P. Mr. Rachleff is also a managing member of Benchmark Capital Management Co., IV, LLC, the general partner of Benchmark Capital Partners, IV, L.P., Benchmark Founders’ Fund IV, L .P. and Benchmark Founders’ Fund IV-A, L.P. In addition, includes 195 shares of common stock and 938 shares subject to options that are exercisable within 60 days of February 28, 2003. |

| (8) | Mr. Volpi is senior vice president of Cisco Systems, Inc., which beneficially holds 212,217 shares of common stock. |

| (9) | Includes 938 shares subject to options that are exercisable within 60 days of February 28, 2003. |

| (10) | Includes 32,658 shares subject to options that are exercisable within 60 days of February 28, 2003. |

| (11) | Includes 21,277 shares subject to options that are exercisable within 60 days of February 28, 2003. |

| (12) | Includes 1,084,686 shares of common stock beneficially owned by i-STT Investments Pte. Ltd., (“i-STTI”) a wholly-owned subsidiary of STT Communications Ltd., and 1,868,667 shares of common stock that may be acquired upon conversion of the Series A Convertible Preferred Stock (“Series A Preferred Stock”) owned by i-STTI. Also includes 1,990,216 shares that may be acquired within 60 days of February 28, 2003 upon conversion of Series A-1 Convertible Secured Notes (the “Notes”) or upon the exercise of Series A-1 Preferred Stock Warrants (the “Warrants”) owned of record by i-STTI. As more fully described in our definitive proxy statement filed with the Securities and Exchange Commission on December 12, 2002 and subject to the qualifications described therein, until December 31, 2004, or if earlier, the termination of the governance provisions in the bylaws, STT and its affiliates may not convert the Notes or exercise the Warrants for shares of our voting stock if such conversion or exercise would cause STT, when combined with shares beneficially held by its affiliates, to beneficially hold more than 40% of our outstanding voting stock. Accordingly, the Notes and Warrants are convertible into or exercisable for shares of common stock or Series A Preferred Stock only to the extent that such exchange will not cause STT or its affiliates to exceed the 40% threshold. If such conversion or exercise would cause STT or its affiliates to exceed the 40% threshold, the Notes and Warrants become convertible or exercisable for shares of non-voting Series A-1 Preferred Stock. |

| (13) | Represents 287,500 shares held by GS Capital Partners 2000, L.P., 104,466 shares held by GS Capital Partners 2000 Offshore, L.P., 12,017 shares held by GS Capital Partners 2000 GmbH & Co. Beteiligungs KG, 91,347 shares held by GS Capital Partners 2000 Employee Fund, L.P., 26,070 shares held by Stone Street Fund 2000, L.P., 147,688 shares held by GS Special Opportunities (Asia) Fund, L.P., 107,668 shares held by GS Special Opportunities (Asia) Offshore Fund, L.P., 173,943 shares held by Whitehall Street Real Estate Limited Partnership XIII, 60,687 shares held by Whitehall Parallel Real Estate Limited Partnership XIII, 5,343 shares held by Stone Street Asia Fund, L.P. and 26,070 shares held by Stone Street Real Estate Fund 2000, L.P. |

| (14) | Includes the shares described in Notes 1 through 11, plus shares held by or subject to options exercisable within 60 days of February 28, 2003 held by executive officers not named above. |

9

COMPENSATION COMMITTEE REPORT

The Compensation Committee has the exclusive authority to establish the level of base salary payable to the chief executive officer (“CEO”) and certain other executive officers of the Company and authority to administer the Company’s 2000 Equity Incentive Plan, 2001 Supplemental Option Plan and Employee Stock Purchase Plan. In addition, the Compensation Committee has the responsibility for approving the individual bonus programs to be in effect for the CEO and certain other executive officers and other key employees each fiscal year.

For the 2002 fiscal year, the process utilized by the Compensation Committee in determining executive officer compensation levels was based on the subjective judgment of the Compensation Committee. Among the factors considered by the Compensation Committee were the recommendations of the CEO with respect to the compensation of the Company’s key executive officers. However, the Committee makes the final compensation decisions concerning such officers.

General Compensation Policy. The Compensation Committee’s fundamental policy is to offer the Company’s executive officers competitive compensation opportunities based upon overall Company performance, their individual contribution to the financial success of the Company and their personal performance. It is the Committee’s objective to have each officer’s compensation reflect his or her own contribution to the Company and level of performance. Each executive officer’s compensation package consists of: (i) base salary, (ii) long-term stock-based incentive awards and (iii) bonuses.

Base Salary. The base salary for each executive officer is set on the basis of general market levels and personal performance. Each individual’s base pay is positioned relative to the total compensation package, including cash incentives and long-term incentives.

Discretionary Bonuses. Due to economic conditions and the Company’s focus on conserving cash, the Company did not have an annual cash bonus program for 2002. Mr. Ferris, the Company’s Vice President of Sales, in the only executive officer who currently has an annual bonus as part of his compensation. Mr. Ferris’ bonus is contingent on his individual performance objectives. For 2002, Mr. Ferris earned a portion of his annual bonus. In addition, Mr. Ferris and Ms. Backaus are entitled to reimbursement of home mortgage interest payments through December 2003 in connection with housing assistance loans they received when they were hired that were subsequently repaid early. In addition, the Company grants one-time discretionary cash or stock bonuses to executive officers for exceptional performance. For 2002, Ms. Lanam and Mr. Taylor were granted cash bonuses for their efforts in completing the combination and financing transactions.

Long-Term Incentive Compensation. During fiscal 2002, the Compensation Committee approved option grants to the executive officers largely in consideration of the challenges facing the Company, high exercise prices for the officers’ existing options and the decision to reduce bonuses in order to conserve corporate cash. Generally, a significant grant is made in the year that an officer commences employment. Thereafter, option grants may be made at varying times and in varying amounts in the discretion of the Compensation Committee. Generally, the size of each grant is set at a level that the Committee deems appropriate to create a meaningful opportunity for stock ownership based upon the individual’s position with the Committee, the individual’s potential for future responsibility and promotion, the individual’s performance in the recent period, the exercise prices of that individual’s outstanding options relative to current market value, and the number of unvested options held by the individual at the time of the new grant. The relative weight given to each of these factors will vary from individual to individual at the Compensation Committee’s discretion.

Each grant allows the officer to acquire shares of the Company’s common stock at a fixed price per share (the market price on the grant date) over a specified period of time. The option vests in periodic installments over a two to four year period, contingent upon the executive officer’s continued employment with the Company. The vesting schedule and the number of shares granted are established to ensure a meaningful incentive in each year following the year of grant. Accordingly, the option will provide a return to the executive officer only if he or she

10

remains in the Company’s employ, and then only if the market price of the Company’s common stock appreciates over the option term.

CEO Compensation. The annual base salary for Mr. Van Camp, the Company’s CEO, was established in connection with his commencement of employment in 2000 and has not been increased since that date. No bonus was paid to the CEO for 2002. An option was granted during fiscal 2002 based on the same factors as for the executive officers.

Tax Limitation. Under the Federal tax laws, a publicly held company such as the Company will not be allowed a federal income tax deduction for compensation paid to certain executive officers to the extent that compensation exceeds $1 million per officer in any year. To qualify for an exemption from the $1 million deduction limitation, the stockholders approved a limitation under the Company’s 2000 Equity Incentive Plan on the maximum number of shares of common stock for which any one participant may be granted stock options per fiscal year. Because this limitation was adopted, any compensation deemed paid to an executive officer when he exercises an outstanding option under the 2000 Equity Incentive Plan with an exercise price equal to the fair market value of the option shares on the grant date will qualify as performance-based compensation that will not be subject to the $1 million limitation. Since it is not expected that the cash compensation to be paid to the Company’s executive officers for the 2002 fiscal year will exceed the $1 million limit per officer, the Compensation Committee will defer any decision on whether to limit the dollar amount of all other compensation payable to the Company’s executive officers to the $1 million cap.

Submitted by the following members of the Compensation Committee:

Scott Kriens

Michelangelo Volpi

COMPENSATION COMMITTEE INTERLOCKS AND INSIDER PARTICIPATION

The Compensation Committee was formed on July 19, 2000 and the current members of the Compensation Committee are Messrs. Eng, Kriens and Volpi. Mr. Eng joined the Compensation Committee in December 2002. None of the members of the Compensation Committee was at any time during the 2002 fiscal year or at any other time an officer or employee of the Company. No executive officer of the Company serves as a member of the board of directors or compensation committee of any entity that has one or more executive officers serving as a member of the Company’s Board of Directors or Compensation Committee.

11

REPORT OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

The Audit Committee serves as the representative of the Board of Directors for general oversight of the Company’s financial accounting and reporting process, system of internal control, audit process, and process for monitoring compliance with laws and regulations and the Company’s Standards of Business Conduct. The Audit Committee annually appoints a firm of independent accountants to audit the financial statements of the Company. A more detailed description of the functions of the Audit Committee can be found in the Company’s Audit Committee Charter, attached to this proxy statement as Appendix A.

From January 1, 2002 to June 7, 2002, the Audit Committee consisted of Messrs. Kriens and Rachleff and Mr. John Taysom. Mr. Taysom resigned from the Board of Directors on June 7, 2002. From June 7, 2002 to December 30, 2002, the Audit Committee consisted of Messrs. Kriens and Rachleff. Mr. Eng joined Messrs. Kriens and Rachleff on the Audit Committee as of December 31, 2002. The Audit Committee held three meetings during the last fiscal year. In addition, the Audit Committee met once in March 2003 to discuss the results of the audit for the last fiscal year.

The Company’s management has primary responsibility for preparing the Company’s financial statements and financial reporting process. The Company’s independent accountants, PricewaterhouseCoopers LLP (“PricewaterhouseCoopers”), are responsible for expressing an opinion on the conformity of the Company’s audited financial statements to generally accepted accounting principles. The Audit Committee serves a board-level oversight role in which it provides advice, counsel and direction to management and the auditors on the basis of the information it receives, discussions with management and the auditors and the experience of the Audit Committee’s members in business, financial and accounting matters.

In this context, the Audit Committee hereby reports as follows:

| • | The Audit Committee has reviewed and discussed the audited financial statements with the Company’s management and the independent auditors. |

| • | The Audit Committee has discussed with the independent accountants the matters required to be discussed by Statement on Auditing Standards No. 61 (Codification of Statements on Auditing Standard, AU 380). |

| • | The Audit Committee discussed with the independent auditor’s the auditor’s independence from the Company and its management. The Audit Committee has received the written disclosures and the letter from the independent accountants required by Independence Standards Board Standard No. 1 (Independence Standards Board Standards No. 1, Independence Discussions with Audit Committees) and has discussed with the independent accountants the independent accountants’ independence. |

Aggregate fees for professional services rendered for the Company by PricewaterhouseCoopers as of or for the years ended December 31, 2002 and 2001, were:

| December 31, | ||||||

| 2002 |

2001 | |||||

| Audit |

$ |

906,000 |

$ |

323,000 | ||

| Audit Related |

|

221,700 |

|

3,500 | ||

| Tax |

|

373,048 |

|

257,759 | ||

| All Other |

|

44,386 |

|

0 | ||

| Total: |

$ |

1,545,134 |

$ |

584,259 | ||

The Audit fees for the years ended December 31, 2002 and 2001, respectively, were for professional services rendered for the audits of the consolidated financial statements of the Company and statutory and subsidiary audits, consents, income tax provision procedures, and assistance with review of documents filed with the SEC.

12

The Audit Related fees as of the years ended December 31, 2002 and 2001, respectively, were for assurance and related services related to employee benefit plan audits, due diligence related to mergers and acquisitions, accounting consultations and audits in connection with acquisitions, and consultations concerning financial accounting and reporting standards.

Tax fees as of the years ended December 31, 2002 and 2001, respectively, were for services related to tax compliance, including the preparation of tax returns; and tax planning and tax advice, including assistance with and representation in tax audits and appeals and advice related to mergers and acquisitions.

All Other Fees were incurred as of the years ended December 31, 2002 and 2001, respectively, were for services rendered for risk management advisory services.

The Company’s Audit Committee has not yet adopted/enacted pre-approval policies and procedures for audit and non-audit services. Therefore, the proxy disclosure does not include pre-approval policies and procedures and related information. The Company is early-adopting components of the proxy fee disclosure requirements; the requirement does not become effective until periodic annual filings for the first fiscal year ending after December 15, 2003.

Based on the Audit Committee’s discussion with management and the independent accountants and the Audit Committee’s review of the representations of management and the report of the independent accountants to the Audit Committee, the Audit Committee and the Board of Directors has approved the audited financial statements and recommended that the audited financial statements be included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2002, for filing with the Securities and Exchange Commission. The Audit Committee and the Board of Directors have also recommended, subject to stockholder approval, the selection of PricewaterhouseCoopers LLP, as the Company’s independent accountants.

Each of the members of the Audit Committee is independent as defined under the listing standards of the Nasdaq National Market.

Submitted by the following members of the Audit Committee:

Scott Kriens

Andrew S. Rachleff

13

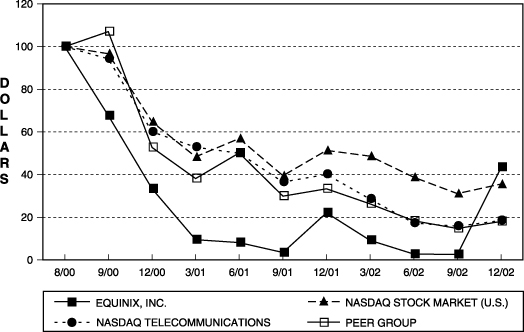

STOCK PERFORMANCE GRAPH

The graph set forth below compares the cumulative total stockholder return on the Company’s common stock between August 11, 2000 (the date the Company’s common stock commenced public trading) and December 31, 2002 with the cumulative total return of (i) the CRSP Total Return Index for the Nasdaq Stock Market (U.S. Companies) (the “Nasdaq Stock Market-U.S. Index”), (ii) the Nasdaq Telecommunications Index and (iii) our peer group of companies which as of the end of our last fiscal year were the companies that comprised the Goldman Sachs Internet Index over the same period. This graph assumes the investment of $100.00 on August 11, 2000, in the Company’s common stock, the Nasdaq Stock Market-U.S. Index, the Nasdaq Telecommunications Index and the Goldman Sachs Internet Index and assumes the reinvestment of dividends, if any.

The comparisons shown in the graph below are based upon historical data. The Company cautions that the stock price performance shown in the graph below is not indicative of, nor intended to forecast, the potential future performance of the Company’s common stock.

COMPARISON OF CUMULATIVE TOTAL RETURN

AMONG EQUINIX, INC., THE NASDAQ STOCK MARKET-U.S. INDEX,

THE NASDAQ TELECOMMUNICATIONS INDEX AND OUR PEER GROUP

The Company effected its initial public offering of common stock on August 11, 2000 at a price of $12.00 per share (without giving effect to the Company’s stock split effective December 31, 2002). The graph above, however, commences with the closing price of $13.125 per share (without giving effect to the Company’s stock split effective December 31, 2002) on August 11, 2000 — the date the Company’s common stock commenced public trading. The closing price of our common stock on December 31, 2002 in the graph above does give effect to the Company’s stock split effective that day.

Notwithstanding anything to the contrary set forth in any of the Company’s previous or future filings under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, that might incorporate this Proxy Statement or future filings made by the Company under those statutes, the Compensation Committee Report and Stock Performance Graph shall not be deemed filed with the Securities and Exchange Commission and shall not be deemed incorporated by reference into any of those prior filings or into any future filings made by the Company under those statutes.

14

EXECUTIVE COMPENSATION AND RELATED INFORMATION

Compensation of Executive Officers

The following table sets forth information with respect to compensation for the fiscal years ended December 31, 2000, 2001 and 2002 paid by the Company for services rendered by the Company’s chief executive officer and the four most highly compensated executive officers whose salary and bonus for the fiscal year ended December 31, 2002 were in excess of $100,000 for services rendered in all capacities to the Company for that fiscal year (collectively, the “Named Executive Officers”):

| Annual Compensation |

Long Term Compensation |

||||||||||||

| Year |

Salary |

Bonus |

Awards Securities Underlying Options (#) |

All Other Compensation (5) | |||||||||

| Peter F. Van Camp (1) |

2002 |

$ |

310,000 |

0 |

|

7,813 |

|

0 | |||||

| Director and Chief Executive Officer |

2001 |

|

308,708 |

873,692 |

(2) |

68,750 |

$ |

109,349 | |||||

| 2000 |

|

194,938 |

1,169 |

|

97,031 |

|

150,000 | ||||||

| Albert M.Avery, IV |

2002 |

|

250,000 |

0 |

|

1,563 |

|

0 | |||||

| Vice Chairman of the Board |

2001 |

|

307,416 |

0 |

|

3,125 |

|

0 | |||||

| 2000 |

|

310,000 |

0 |

|

1,7500 |

|

0 | ||||||

| Marjorie S. Backaus |

2002 |

|

225,000 |

29,946 |

(3) |

4,688 |

|

0 | |||||

| Chief Marketing Officer and |

2001 |

|

221,562 |

41,132 |

|

14,843 |

|

0 | |||||

| Vice President of Market Strategy |

2000 |

|

200,781 |

4,328 |

|

1,750 |

|

51,789 | |||||

| Peter F. Ferris |

2002 |

|

205,000 |

99,110 |

(4) |

4,688 |

|

0 | |||||

| Vice President, Worldwide Sales |

2001 |

|

202,244 |

62,572 |

|

14,843 |

|

0 | |||||

| 2000 |

|

192,995 |

64,157 |

|

1,750 |

|

0 | ||||||

| Renee F. Lanam |

2002 |

|

230,500 |

80,000 |

|

10,157 |

|

0 | |||||

| Chief Financial Officer, Secretary |

2001 |

|

214,083 |

1,015 |

|

14,845 |

|

0 | |||||

| 2000 |

|

138,223 |

1,234 |

|

11,798 |

|

0 | ||||||

| (1) | Mr. Van Camp joined the Company in May 2000. |

| (2) | Represents the partial forgiveness of an employee loan in exchange for Mr. Van Camp waiving his right to any bonuses earned and expensed in 2001. |

| (3) | Represents interest payments on a home loan pursuant to early repayment agreements. See “Certain Relationships and Related Transactions—Loans to Executive Officers” for a description of such repayment agreements. |

| (4) | Includes $59,110 in interest payments on a home loan pursuant to early repayment agreements. See “Certain Relationships and Related Transactions—Loans to Executive Officers” for a description of such repayment agreements. |

| (5) | Except as otherwise noted, All Other Compensation reflects payment of relocation expenses. |

15

Stock Option Grants

The following table shows for the year ended December 31, 2002, certain information regarding options granted to the Named Executive Officers:

| Potential Realizable Value at Assumed Annual Rates of Stock Price Appreciation for Option Term(4)($) | ||||||||||||||||

| Name |

Number of Securities Underlying Options granted (#)(1) |

% of Total Options Granted to Employees in 2002 (2) |

Exercise or Base Price ($/sh)(3) |

Expiration Date |

5% |

10% | ||||||||||

| Peter F. Van Camp |

7,813 |

5.60 |

% |

$ |

22.40 |

4/22/2012 |

$ |

110,064 |

$ |

278,923 | ||||||

| Albert M. Avery, IV |

1,563 |

1.12 |

% |

$ |

22.40 |

4/22/2012 |

|

22,018 |

|

55,799 | ||||||

| Marjorie S. Backaus |

4,688 |

3.36 |

% |

$ |

22.40 |

4/22/2012 |

|

66,041 |

|

167,361 | ||||||

| Peter Ferris |

4,688 |

3.36 |

% |

$ |

22.40 |

4/22/2012 |

|

66,041 |

|

167,361 | ||||||

| Renee F. Lanam |

4,688 |

3.36 |

% |

$ |

51.20 |

2/19/2012 |

|

150,951 |

|

382,539 | ||||||

| 5,469 |

3.92 |

% |

$ |

22.40 |

4/22/2012 |

|

77,043 |

|

195,242 | |||||||

| (1) | The options in the table that show an expiration date of February 19, 2012 were granted on February 19, 2002 and the options in the table that show an expiration date of April 22, 2012 were granted on April 22, 2002. These options are exercisable in 48 equal monthly installments from the grant date. The plan administrator has the discretionary authority to re-price the options through the cancellation of those options and the grant of replacement options with an exercise price based on the fair market value of the option shares on the re-grant date. The options have a maximum term of 10 years measured from the option grant date, subject to earlier termination in the event of the optionee’s cessation of service with the Company. Under each of the options, the option shares vest upon an acquisition of the Company by merger or asset sale, unless the acquiring entity or its parent corporation assumes the outstanding options. Any options which are assumed or replaced in the transaction and do not otherwise accelerate at that time automatically accelerate (and any unvested option shares which do not otherwise vest at that time automatically vest) in the event the optionee’s service terminates by reason of an involuntary or constructive termination within 18 months following the transaction. |

| (2) | Based on an aggregate of 139,618 shares subject to options granted in the fiscal year ended December 31, 2002. |

| (3) | The exercise price for each option may be paid in cash, in shares of common stock valued at fair market value on the exercise date or through a cashless exercise procedure involving a same-day sale of the purchased shares. The Company may also finance the option exercise by loaning the optionee sufficient funds to pay the exercise price for the purchased shares, together with any federal and state income tax liability incurred by the optionee in connection with such exercise. |

| (4) | In accordance with the rules of the Securities and Exchange Commission (“SEC”), the table sets forth the hypothetical gains or “option spreads” that would exist for the options at the end of their respective ten-year terms based on assumed annualized rates of compound stock price appreciation of 5% and 10% from the dates the options were granted to the end of the respective option terms. Actual gains, if any, on option exercises are dependent on the future performance of the Company’s common stock and overall market conditions. There can be no assurance that the potential realizable values shown in this table will be achieved. |

16

Aggregate Option Exercises in 2002 and Fiscal Year-End Option Values

No options were exercised by the Named Executive Officers in 2002. The following table sets forth for each of the Named Executive Officers the number and value of securities underlying options held by the Named Executive Officers at December 31, 2002:

| Name |

Number of Securities Underlying Unexercised Options at |

Value of Unexercised In-The-Money Options at December 31, 2002 (1) | ||||||||

| Exercisable |

Unexercisable |

Exercisable |

Unexercisable | |||||||

| Peter F. Van Camp |

132,189 |

41,407 |

$ |

0 |

$ |

0 | ||||

| Albert M. Avery, IV |

3,703 |

2,735 |

$ |

0 |

$ |

0 | ||||

| Marjorie S. Backaus |

21,005 |

10,825 |

$ |

0 |

$ |

0 | ||||

| Peter Ferris |

10,458 |

10,825 |

$ |

0 |

$ |

0 | ||||

| Renee F. Lanam |

19,528 |

15,318 |

$ |

0 |

$ |

0 | ||||

| (1) | Based on the fair market value of the Company’s common stock as of December 31, 2002 ($5.70 per share), minus the exercise price, multiplied by the number of shares underlying the options. |

Employment Agreements, Change of Control Arrangements and Severance Agreements

The Compensation Committee, as plan administrator of the 2000 Equity Incentive Plan, has the authority to provide for accelerated vesting of the shares of common stock subject to outstanding options held by the Named Executive Officers and any other person in connection with certain changes in control of Equinix. In connection with the adoption of the 2000 Equity Incentive Plan, the Company has provided that upon a change in control of the Company, each outstanding option and all shares of restricted stock will generally become fully vested unless the surviving corporation assumes the option or award or replaces it with a comparable award. Any options which are assumed or replaced in the transaction and do not otherwise accelerate at that time shall automatically accelerate (and any unvested option shares which do not otherwise vest at that time shall automatically vest) in the event the optionee’s service terminates by reason of an involuntary or constructive termination within 18 months following the transaction. In addition, options granted to the executive officers of the Company prior to the Company’s initial public offering provide for an additional 12 months vesting upon a change in control of the Company and our form of offer letter for officers provides for an additional 12 months of vesting upon a change in control, provided such officer is employed upon the closing of the change in control. Except as noted below, none of the Company’s executive officers have employment agreements with the Company, and their employment may be terminated at any time.

In August 2002, the Company entered into Severance Agreements with its executive officers, Peter Van Camp, Marjorie S. Backaus, Peter Ferris, Philip J. Koen, Renee Lanam, and Keith Taylor. The agreements provide for severance payments equal to the officer’s annual base salary and target bonus in the event such officer’s employment is terminated for any reason other than cause or the officer resigns for good reason as defined in the agreement.

The initial stock option agreement for Peter F. Van Camp, the Company’s chief executive officer, provides that he will vest an additional 12 months in his initial option upon a change in control of the Company.

The Company extended an offer of employment to Marjorie S. Backaus, the Company’s Chief Marketing Officer, pursuant to an offer letter dated October 21, 1999. The agreement provides that she will vest an additional 12 months in her options upon a change in control of the Company.

The Company extended an offer of employment to Peter T. Ferris, the Company’s vice president, worldwide sales, pursuant to an offer letter dated June 28, 1999. The letter provides for acceleration of vesting of option shares for an additional 12 months if there are certain changes in control of the Company.

17

The Company entered into an agreement on February 8, 2000 with Albert M. Avery, IV, its former vice chairman of the Board of Directors, which provides that his base compensation will be the same as the CEO’s base compensation and also provides for continuation of his salary and continued option vesting for 12 months should his employment with the Company cease. Any options granted to Mr. Avery after February 8, 2000 will allow 24 months to exercise post-termination of employment. On January 1, 2003, the Company entered into an agreement with Albert M. Avery IV relating to his cessation of employment with the Company effective January 6, 2003. Under the agreement, Mr. Avery received severance benefits consisting of a lump sum cash payment of $311,292 pursuant to the terms of his existing employment contract, plus $9,554.52 in payment of COBRA premiums, payment of legal fees to Mr. Avery’s counsel, and a personal computer, blackberry, and cell phone used by Mr. Avery while employed by the Company. In addition, he will continue to vest in his stock options through December 31, 2003 and will have two years to exercise vested options. The agreement also contains certain restrictive covenants, mutual releases and other customary terms and conditions.

18

PROPOSAL 2

RATIFICATION OF INDEPENDENT ACCOUNTANTS

The Company is asking the stockholders to ratify the appointment of PricewaterhouseCoopers LLP as the Company’s independent accountants for the fiscal year ending December 31, 2003. The affirmative vote of the holders of a majority of shares present or represented by proxy and voting at the Annual Meeting will be required to ratify the appointment of PricewaterhouseCoopers LLP.

In the event the stockholders fail to ratify the appointment, the Board of Directors will reconsider its selection. Even if the appointment is ratified, the Audit Committee, in its discretion, may direct the appointment of a different independent accounting firm at any time during the year if the Audit Committee feels that such a change would be in the Company’s and its stockholders’ best interests.

PricewaterhouseCoopers LLP has audited the Company’s financial statements since 2000. Its representatives are expected to be present at the Annual Meeting, will have the opportunity to make a statement if they desire to do so, and will be available to respond to appropriate questions.

Recommendation of the Board of Directors

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” PROPOSAL 2.

PROPOSAL 3

ISSUANCE OF SHARES IN DEBT FINANCING

Background of the Financing

In recent years, as a part of the continuous evaluation of our business, we have regularly considered a variety of strategic initiatives and transactions with a view toward increasing stockholder value. In this regard, we have explored different strategic alternatives, including the consideration of acquisitions, dispositions and commercial relationships. As a result of these efforts, in December 2002 we issued and sold convertible secured notes and warrants to i-STT Investments Pte Ltd, an affiliate of STT Communications (the “December Financing”) pursuant to a Securities Purchase Agreement dated October 2, 2002, as amended (the “Securities Purchase Agreement”). The December Financing, including a description of the convertible secured notes and warrants, is more fully described in the Company’s definitive proxy statement dated December 12, 2002 (the “December Proxy”). At the meeting held in connection with the December Proxy, we obtained stockholder approval for a financing of up to $40 million in exchange for convertible secured notes and warrants under the terms described in the December Proxy. Ultimately, we issued $30 million in convertible secured notes and warrants in the December Financing.

Beginning in late 2002, we, together with our advisors, met with Crosslink Captial (“Crosslink”) numerous times to discuss the terms and conditions of a possible financing transaction. In early February 2003, Crosslink presented a term sheet to the company to invest $10.0 million in the form of convertible secured notes. Throughout February and March 2003, Crosslink met with officers of the Company and conducted extensive due diligence.

On March 6, 2003, our board of directors held a regular meeting during which our board of directors reviewed the proposed term sheet and the general structure of the proposed financing transaction. Following a full discussion, our board of directors determined that the proposed investment by Crosslink is fair to, and in the best interests of, our stockholders and approved the financing and related matters, and authorized our management to finalize the documentation for this financing.

19

On April 15, 2003, our board of directors held a special meeting during which our board of directors considered modifications to the terms of the Crosslink Financing (as defined below) and determined that the modified investment by Crosslink remains fair to, and in the best interests of, our stockholders.

On April 29, 2003, the parties executed and delivered the securities purchase and admission agreement.

We are now seeking stockholder approval for the sale and issuance to Crosslink of $10.0 million of convertible secured notes and warrants not sold in the December Financing (the “Crosslink Financing”). The notes and warrants issued to Crosslink will be convertible into shares of our common stock. If all of such notes and warrants were converted into shares of our common stock, such shares, in the absence of note and warrant conversions by i-STT Communications, could represent greater than 20% of our outstanding common stock. In addition, the convertible secured notes and warrants proposed to be issued in the Crosslink Financing will have materially different terms with respect to their conversion into our common stock than the notes and warrants approved in the December Financing. Therefore, because the notes will have different terms than those approved in connection with our December Financing and because the shares issuable upon conversion of the notes and warrants into common stock could exceed 20% of our outstanding common stock, we are required under the rules of the Nasdaq National Market to seek stockholder approval for the issuance of notes and warrants to Crosslink. See “Terms of the Debt Financing” below.

Our Reasons for the Financing

Our board of directors believes that the terms of the Crosslink Financing transaction are in our best interests and the interests of our stockholders. Accordingly, at a meeting held on March 6, 2003, our board of directors approved the transaction and recommended that our stockholders approve the issuance of shares of our common stock in connection with the Crosslink Financing. In reaching its determination, our board of directors consulted with our management and advisors, and carefully evaluated the financial terms of the transaction agreements and their effect on the holders of our preferred stock and common stock. Specifically, our board of directors considered the increased financial stability and greater operating flexibility provided by raising additional cash. Our board of directions believes that this value warrants the additional dilution to existing stockholders.

Why We Need Stockholder Approval of the Financing

You are entitled to vote on the approval of the proposed issuance because the securities to be issued are convertible into our common stock which is qualified to trade on The Nasdaq National Market, and the rules of the Nasdaq National Market require us to seek the approval of our stockholders prior to the issuance of securities in connection with a transaction (other than a public offering) involving our sale or issuance of common stock (or securities convertible into or exercisable for common stock) equal to 20% or more of the common stock or 20% or more of the voting power outstanding, for less than the greater of book value or market value of the common stock before such issuance (the “Nasdaq 20% Rule”). Accordingly, we are seeking stockholder approval in order to ensure compliance with the Nasdaq 20% Rule, which is required to maintain our listing on the Nasdaq National Market. Stockholder approval of the issuance is not otherwise required as a matter of Delaware law or other applicable laws or rules, or by our Restated Certificate of Incorporation, as amended, or by our bylaws.

Interests of Our Directors and Executive Officers

When considering the recommendation of our board of directors that stockholders approve the issuance of shares of common stock in the Crosslink Financing, you should be aware that some of our directors and executive officers have interests in these transactions that are different from, or are in addition to, your interests. Our board of directors was aware of these potential conflicts and considered them. These include:

Directors. Each of the directors nominated for election at this meeting will remain on our board of directors following the closing of the Crosslink Financing. Mr. Dennis Raney was not a member of our board of directors at the March 6, 2003 meeting where the Crosslink Financing was approved.

20

Indemnification of Directors and Officers. Our executive officers and directors have customary rights to indemnification against losses incurred as a result of action or omission occurring prior to the closing. In addition, our executive officers and directors have customary indemnification agreements that provide for additional indemnification.

Anti-dilution Protection for i-STT Investments Pte. Ltd. As more fully described below, under the terms of the note issued to i-STT Investments, an affiliate of STT Communications, in the December Financing, the rate at which such note converts into our capital stock will be adjusted to protect i-STT Investments from some of the dilutive effects of the investment by Crosslink. Lee Theng Kiat and Jean Mandeville, two of the Company’s directors, are executive officers of STT Communications.

As a result, these directors and executive officers could be more likely to vote in favor of recommending the issuance of shares of common stock in the financing than if they did not hold these interests.

Terms of the Debt Financing

Securities to be Issued. The following securities will be issued under the securities purchase and admission agreement:

| • | Series A-2 convertible secured notes due November 1, 2007 with an aggregate principal amount of $10.0 million; |

| • | warrants to purchase shares of our common stock; |

| • | warrants to purchase shares of our common stock upon a change of control; and |

| • | warrants to purchase shares of our common stock upon defaults under our senior credit facility. |

Closing Conditions. The issuance and sale of securities in the Crosslink Financing is subject to closing conditions, including:

| • | the amendment of Article VII of our bylaws to provide for the nomination of one (1) director designated by Crosslink at each election of our board of directors until such Article terminates in accordance with its terms; |

| • | the approval of our stockholders of the issuance of securities pursuant to the securities purchase and admission agreement; and |

| • | the resolution of potential obligations by us to STT Communications regarding outstanding bank guarantees to the satisfaction of Crosslink. |

Representations and Warranties; Indemnities and Expenses. The securities purchase and admission agreement includes representations and warranties and incorporates the affirmative and negative covenants and events of default under our credit facility. We will indemnify the holders of the convertible secured notes from specific liabilities, such as environmental liabilities. In addition, we will reimburse $75,000 of fees of counsel to the purchasers under the securities purchase and admission agreement.

Registration Rights. Crosslink will become party to the registration rights agreement we entered into with i-STT Investments which has been amended to grant the right to five demand registrations, the right to participate in other registration statements filed by us (other than employee stock and acquisition related offerings) and the right to register shares on Form S-3 (or Form S-1 if Form S-3 is not available) shares of our common stock issued, directly or indirectly, upon conversion of the notes or exercise of any of the warrants issued under the securities purchase and admission agreement. The registration rights agreement includes our obligation to indemnify or contribute to losses suffered by the holders of securities registered pursuant to that agreement. These losses may include losses incurred under federal securities laws.

21

Nomination of Directors. Under the provisions of the Bylaws, the number of directors is fixed at nine. The Bylaws currently provide that, until December 31, 2004, or if earlier, the termination of the governance provisions in our bylaws (i) three directors shall be nominated by i-STT Investments, (ii) three directors, known as the Equinix directors, shall be nominated by the three directors appointed to Equinix’s current board of directors by Equinix’s board of directors as it existed prior to December 31, 2002, (iii) prior to May 30, 2003, one director shall be nominated by the former stockholders of Pihana Pacific, Inc. which we acquired on December 31, 2002, and (iv) two directors shall be independent directors nominated by our nominating committee. In connection with the Crosslink Financing, we are required, as a condition to closing, to amend our Bylaws to remove the now obsolete requirement to elect a representative of the former Pihana Pacific stockholders and insert a requirement to nominate a designee of Crosslink. Crosslink will continue to have the right to nominate such director until December 31, 2004, or if earlier, the termination of the governance provisions in the bylaws. Our existing governance provisions are more fully described in our definitive proxy statement dated December 12, 2002.

The Series A-2 Convertible Secured Notes

Principal Amount. Under the securities purchase and admission agreement, Crosslink has committed to purchase an aggregate principal amount of $10.0 million of Series A-2 convertible secured notes.

Security. The Series A-2 convertible secured notes share with our existing Series A-1 convertible secured notes a second priority security interest in all of the collateral securing our and our subsidiaries’ obligations under the credit facility (which excludes the i-STT assets and Pihana’s Singapore assets we purchased on December 31, 2002).

The Series A-2 convertible secured notes will be guaranteed by all of our existing subsidiaries, all of our subsidiaries acquired in the combination (except that the Singapore subsidiaries will guarantee only our previously issued Series A-1 convertible secured notes) and all of our future domestic subsidiaries.

Interest. Interest will begin to accrue on the Series A-2 convertible secured notes at the rate of 10% per year two years after the date of issuance of the Series A-2 convertible secured notes. Interest on the Series A-2 convertible secured notes will be payable in arrears in additional notes of the same series, on May 1 and November 1 of each year, beginning on November 1, 2005 until maturity.